We find ourselves in yet another tale of two markets this year. The tech-heavy Nasdaq is up nearly 30% year-to-date, whereas the blue-chip-heavy Dow was flat through May—the widest spread in nearly 40 years.

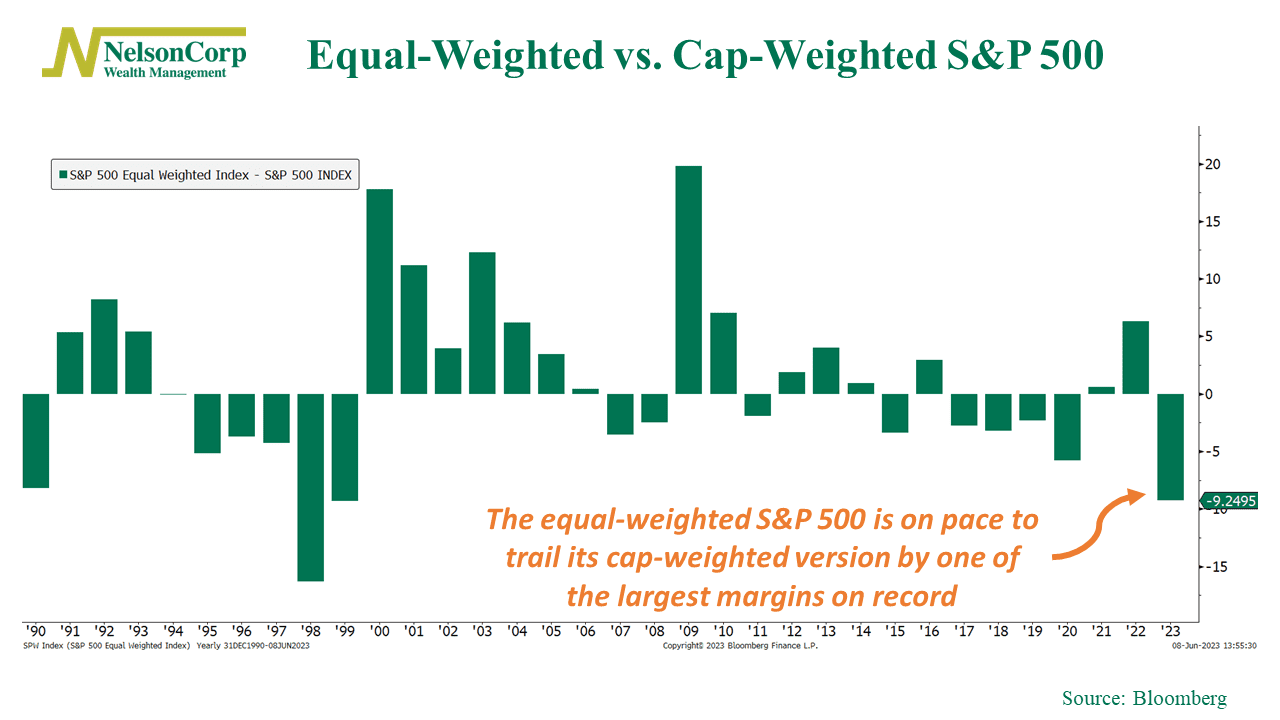

Another way to view how narrow this market rally has been is to look at the equal-weighted version of the S&P 500 Index—which gives every S&P 500 stock an equal weight in the index—versus its regular cap-weighted version. The spread between these two indices is shown on our featured chart above.

Compared to the traditional index’s 12% gain this year, the equally weighted version has added just 2.5%, resulting in a year-to-date spread of about -9.5%. That is the largest-ever underperformance for the equal-weight version on a year-to-date basis since data started in 1990. For a full calendar year, as the chart shows, the largest underperformance occurred in 1998, just before the Dot-com bubble burst.

In other words, the majority of this year’s stock market gains have come from just a few, very large companies. Although you can see from the chart that narrow leadership by the biggest companies isn’t unusual, the fact that we are already nearing record-low underperformance for the equal-weight index after just half a year does make the current market environment look a bit extreme.

The important thing to remember is that stocks rarely follow an uninterrupted path upward. Sometimes a few large stocks can manage to keep the market afloat, and other times they fail and end up pulling the market under with them.

There’s a lot to be excited about year-to-date, but we should always be prepared and expect a few bumps along the way as we attempt to climb out of this bear market.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.