OVERVIEW

Markets delivered a mixed but generally positive week, with leadership shifting toward smaller companies and value-oriented stocks. The S&P 500 rose 0.27%, while the Dow Jones Industrial Average outperformed with a 1.53% gain. The NASDAQ slipped 0.58%, weighed down by weakness in growth stocks. Small- and mid-caps surged, with the S&P 600 climbing 3.46% and the S&P 400 up 2.63%, both reversing prior underperformance. Value once again led the way, as the Russell 3000 Value advanced 1.88% versus a 0.70% decline in the Russell 3000 Growth.

International equities continued to add support. Developed markets (EAFE) gained 0.80%, while emerging markets pulled back 0.46%. The U.S. dollar was little changed, down just 0.04% for the week.

Bond markets posted modest gains across most maturities. Short-term Treasuries were flat to slightly higher at 0.09%, intermediate Treasuries gained 0.41%, and long-term Treasuries advanced 0.73%. Investment-grade corporates rose 0.36%, high yield bonds added 0.27%, and municipal bonds ticked up 0.16%. Inflation-protected securities (TIPS) were stronger, climbing 0.80%.

Commodities rallied broadly. Oil gained 2.53%, gold added 1.06%, and corn rebounded with a 1.54% increase. Real estate also showed strength, up 2.80%. Volatility eased further, with the VIX falling 5.77% to its lowest levels of the year.

KEY CONSIDERATIONS

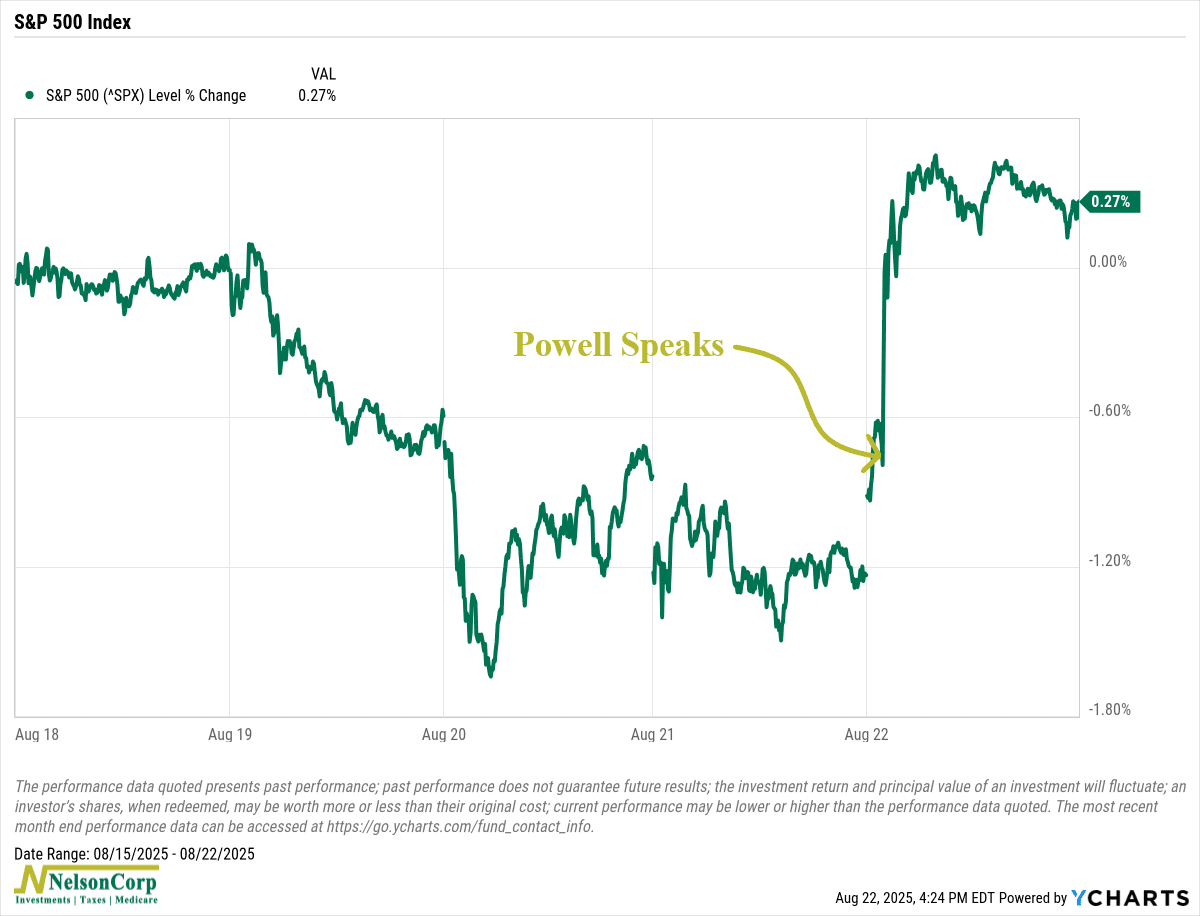

Friendlier Fed – A lot of people were looking forward to the end of last week. And no, it wasn’t just because college football was kicking off (though plenty of us are excited about that too). In the financial world, the real excitement was all about Jerome Powell’s final speech at the annual Jackson Hole conference in Wyoming.

I’ll spare you the details of the speech, but the main takeaway was that because we’ve seen a downturn in the job market, the Fed is now open to the idea of cutting rates as soon as its meeting next month.

Naturally, stocks cheered the news. The S&P 500, our benchmark for U.S. stock returns, jumped 1.5% that day alone. For the week, the index ended up 0.3%, reversing what had been shaping up to be a down week.

Why such bullishness? Because the last time the Fed cut rates was way back in December 2024. At that point, policymakers lowered the Fed Funds Rate—the overnight rate at which banks lend to each other—to a range of 4.25%–4.50%. Then they paused, waiting to see what would happen with inflation.

And for the most part, inflation has behaved. But now, with the labor market softening, cuts are back on the table. So the big question is, what happens when the Fed actually starts cutting again?

History gives us a pretty good hint. Looking back at the seven most recent cycles when the Fed paused for six months or more and then cut again, the stock market has done very well.

As you can see from the chart above, on average, the S&P 500 has risen over 15% in the subsequent 12 months after the Fed’s first cut after a pause. And interestingly enough, if you look at the months before the first cut (the period to the left of the vertical dashed line), the stock market looks eerily similar to this year: A deep sell-off 5-7 months before the first cut, followed by a strong rally in the months leading up to the cut.

So yeah, you can see why stocks cheered Powell’s speech. But exactly how much will the Fed cut rates once it begins again? Well, if we look at the “real” Fed Funds Rate—meaning the rate after backing out inflation—we see that policy has been pretty restrictive.

As this last chart shows, the Fed has a longer-run real rate target (what they call the neutral rate) of 1.0%. But currently, it’s running around 1.65%, which is roughly one whole standard deviation above the target.

That gap suggests there could be room for as many as three rate cuts, depending on how the data unfolds. And as the chart above shows, when the real rate drifts closer to neutral, stocks have historically performed even better.

So, I’ll wrap this all up and say that the bottom line is that investors now have reason to expect a friendlier Fed going forward. And if history is any guide, that could mean more tailwinds for stocks in the months ahead.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The S&P 500 Index, or Standard & Poor’s 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.