OVERVIEW

Markets rallied across the board last week, with major indexes posting strong gains. The S&P 500 climbed 3.44%, the Dow added 3.82%, and the NASDAQ surged 4.25%. Small- and mid-cap stocks also participated, with the S&P 400 up 2.56% and the S&P 600 advancing 3.10%. Growth stocks led the charge, as the Russell 3000 Growth Index jumped 4.39%, outpacing the 2.17% gain in Value.

International equities had a solid showing as well. Developed markets (EAFE) rose 3.05%, while emerging markets climbed 3.25%. The U.S. dollar weakened again, falling 1.39% on the week.

Bonds posted modest gains. Treasuries were positive across the curve, with short-term up 0.10%, intermediate-term up 0.62%, and long-term up 1.03%. Investment-grade corporates gained 0.67%, high yield rose 0.81%, and municipals edged up 0.35%.

Commodities stumbled. Oil plunged 11.84%, dragging the broader commodity index down 3.61%. Gold slipped 2.90%, and corn fell 3.29%. Real estate declined 1.49%, and MLPs were flat. The VIX dropped sharply by 20.85%, reflecting easing investor anxiety.

KEY CONSIDERATIONS

The Big Picture – Shhh… hear that? That was the sound of the market knocking on the door of new highs last week.

And after Friday’s close, it walked right through.

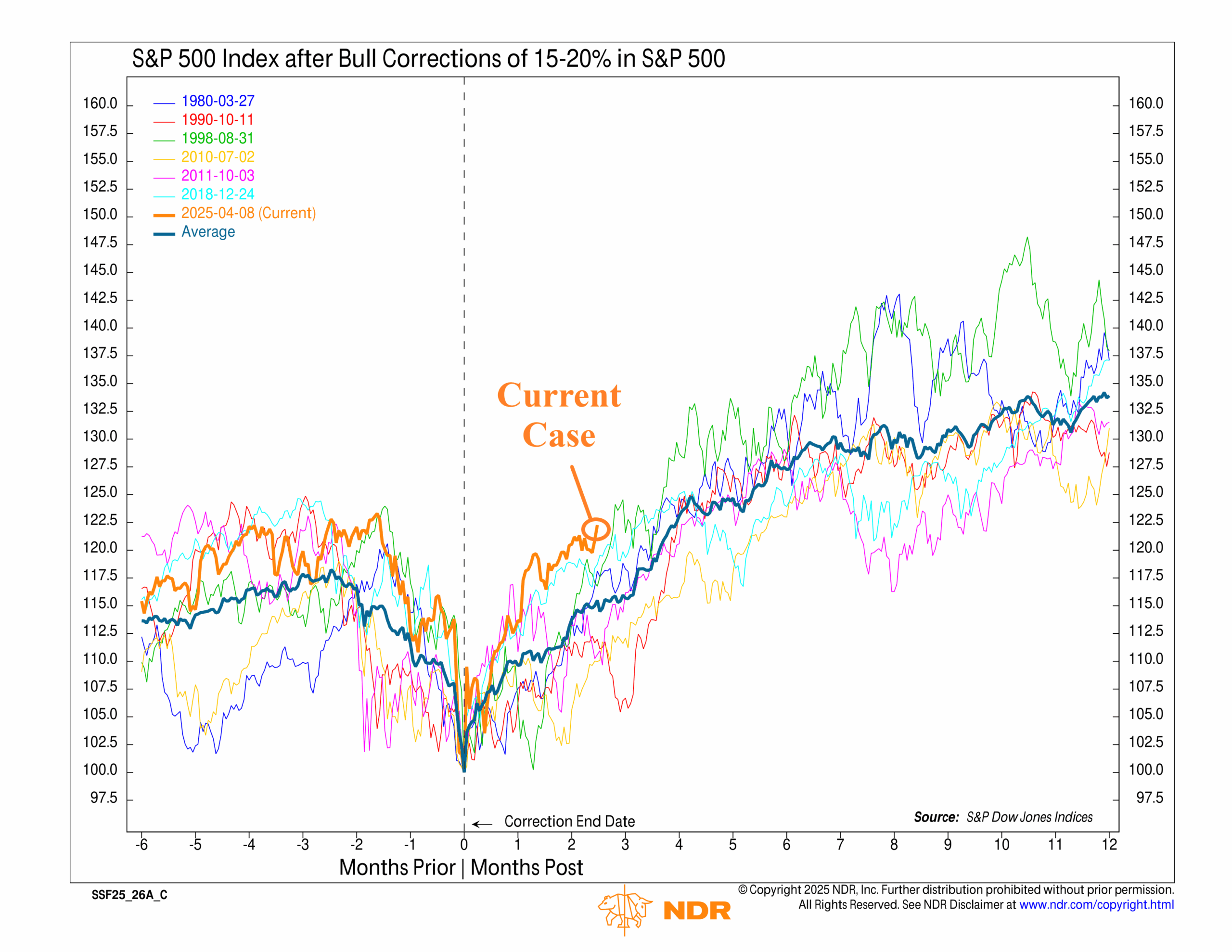

But for real, the rally since the April drawdown has been impressive. As this week’s Chart of the Week showed, it’s actually the strongest rebound on record following a 15–20% correction.

So, where do our models stand after a move like that? Pretty good, actually. We’re sitting at more than 60% bullish—a solid, constructive reading, but not euphoric. Most of that strength is still coming from Market Action, our proxy for price momentum, which remains in great shape.

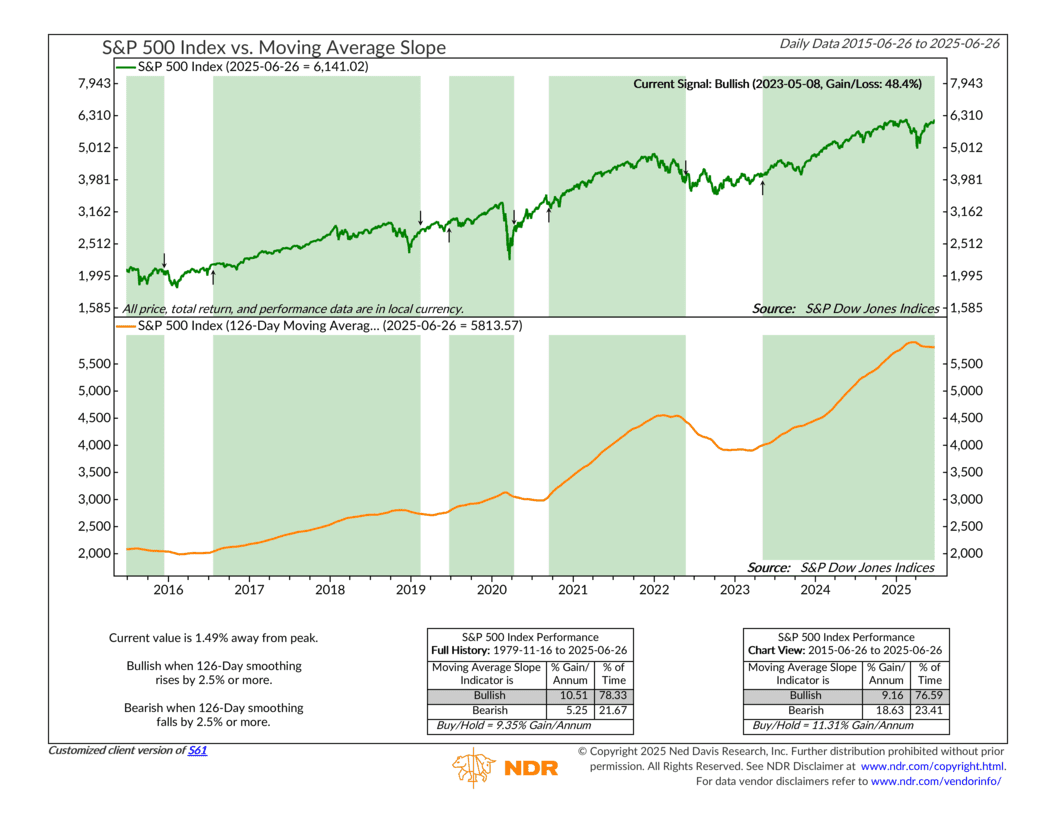

From a technical perspective, the S&P 500’s 126-day moving average slope (shown below) dipped about 1.5% during April’s decline but never broke trend. The longer-term uptrend remains intact, and it’s still pointing higher.

Investor Behavior, on the other hand, looks a bit more mixed. There’s been some pickup in risk-taking—particularly in the leveraged ETF space—which is encouraging. But overall sentiment remains pretty neutral.

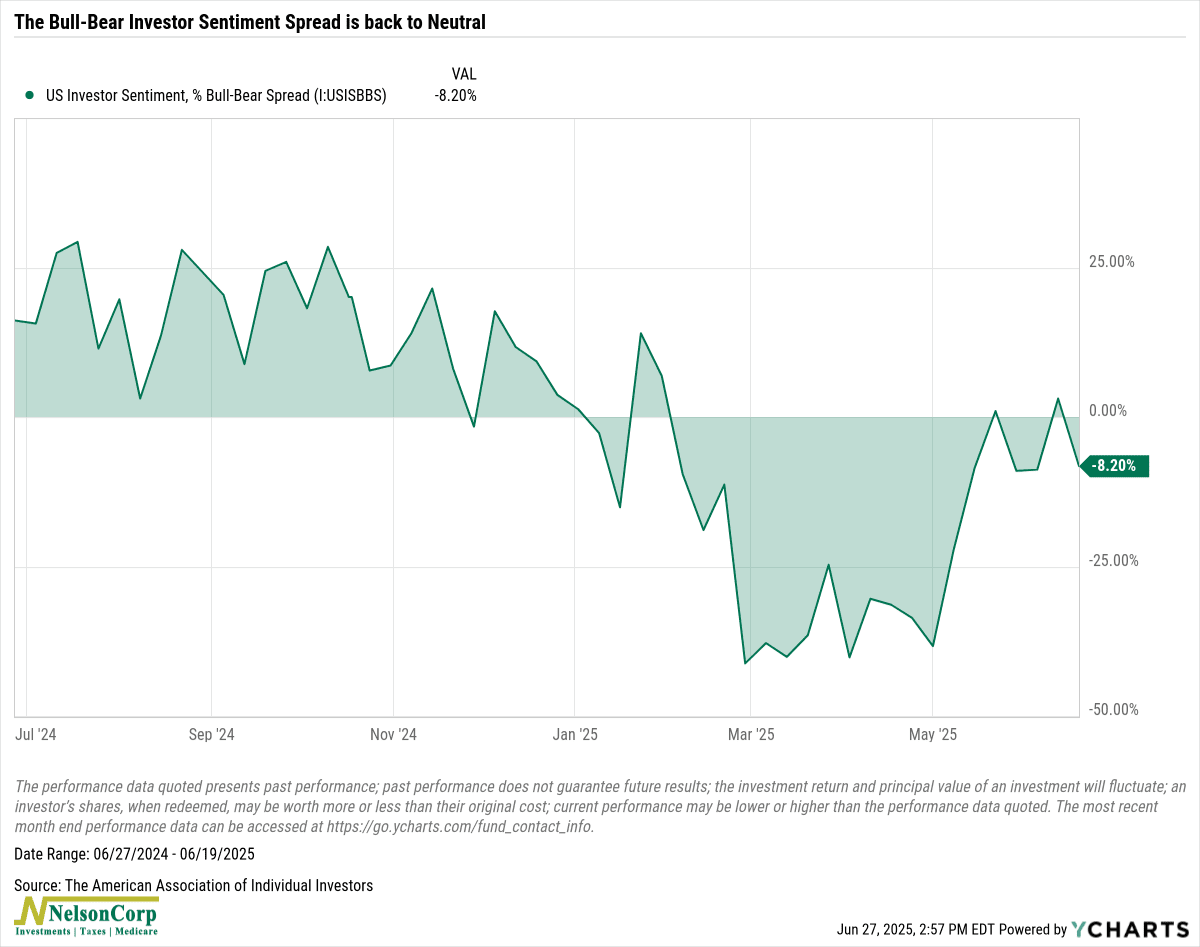

The Bull-Bear Spread (shown below) is back to neutral territory after hitting a low in April. But that’s actually a good sign. We’re not in euphoric territory, but we’ve also shaken off the worst of the pessimism. That’s often fertile ground for bull markets.

And finally, the macro picture is still a mixed bag. We continue to see improvement in liquidity and inflation trends, but economic activity continues to underwhelm.

One example: the Citigroup Economic Surprise Index (shown below) is still stuck in a downtrend from its November 2024 high, with little sign of turning higher in a meaningful way.

We’re also seeing signs of softening in the labor market. Payroll growth has cooled, and job openings continue to drift lower, which adds to the sense that economic momentum is losing steam.

Taken together, it’s a market that still leans positive—but not without a few question marks.

The market environment remains green. Technicals look strong, and sentiment and macro conditions are supportive enough to keep the rally going.

But let’s not forget: breaking and entering can come with risks. The bulls may have forced their way to new highs, but they’ll need more support from the investor behavior and macro side if they want to stick around.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The S&P 500 Index, or Standard & Poor’s 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.