OVERVIEW

Markets stumbled last week, with losses across most major asset classes. The S&P 500 fell 2.36%, while the Dow dropped 2.92%. The NASDAQ declined 2.17%, giving back some of its recent gains. Mid- and small-cap stocks took a bigger hit, with the S&P 400 down 3.53% and the S&P 600 off 3.95%. Value stocks lagged behind, as the Russell 3000 Value Index fell 3.21%, worse than the 1.81% decline in Growth.

International stocks didn’t fare much better. Developed markets (EAFE) sank 3.14%, and emerging markets slipped 2.51%. The U.S. dollar climbed 1.40% for the week.

Bonds were one of the few bright spots. Long-term Treasuries gained 2.02%, intermediate-term Treasuries rose 1.02%, and short-term Treasuries added 0.12%. Investment-grade bonds advanced 0.84%, while high yield dipped slightly, down 0.16%. Municipal bonds also edged higher, up 0.47%.

Commodities struggled. Oil was a notable exception, jumping 3.49%, but gold inched up just 0.22%, and corn dropped 2.50%. Real estate slid 3.06%. Meanwhile, volatility spiked, with the VIX surging to over 20, a sign of rising investor nervousness.

KEY CONSIDERATIONS

How’s the Market Doing? – “How’s the market doing?”

It’s a question we get all the time. And lately, the answer has been: pretty good.

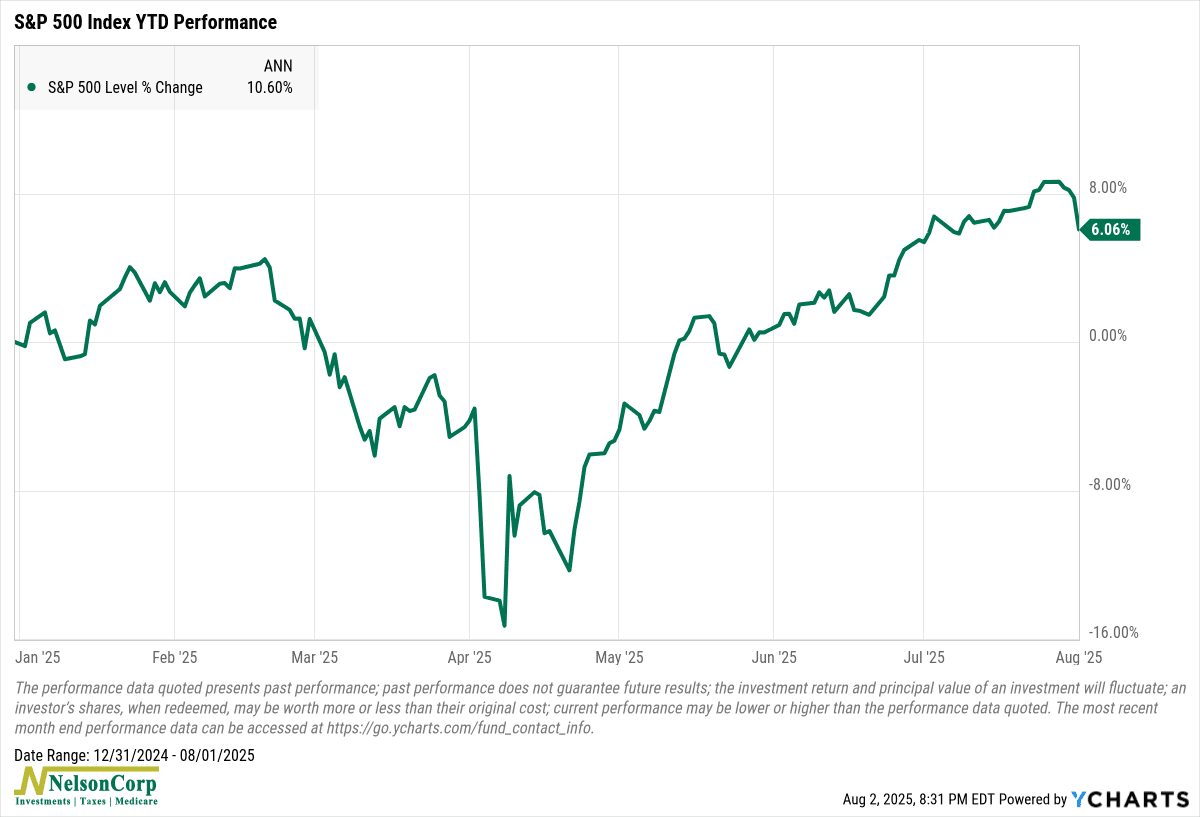

If we look at our standard benchmark for U.S. stock returns—the S&P 500—it’s up around 6% year-to-date. That’s not bad. On an annualized basis, that works out to around 10-11%. Also not bad, especially considering the sharp sell-off we saw earlier this year.

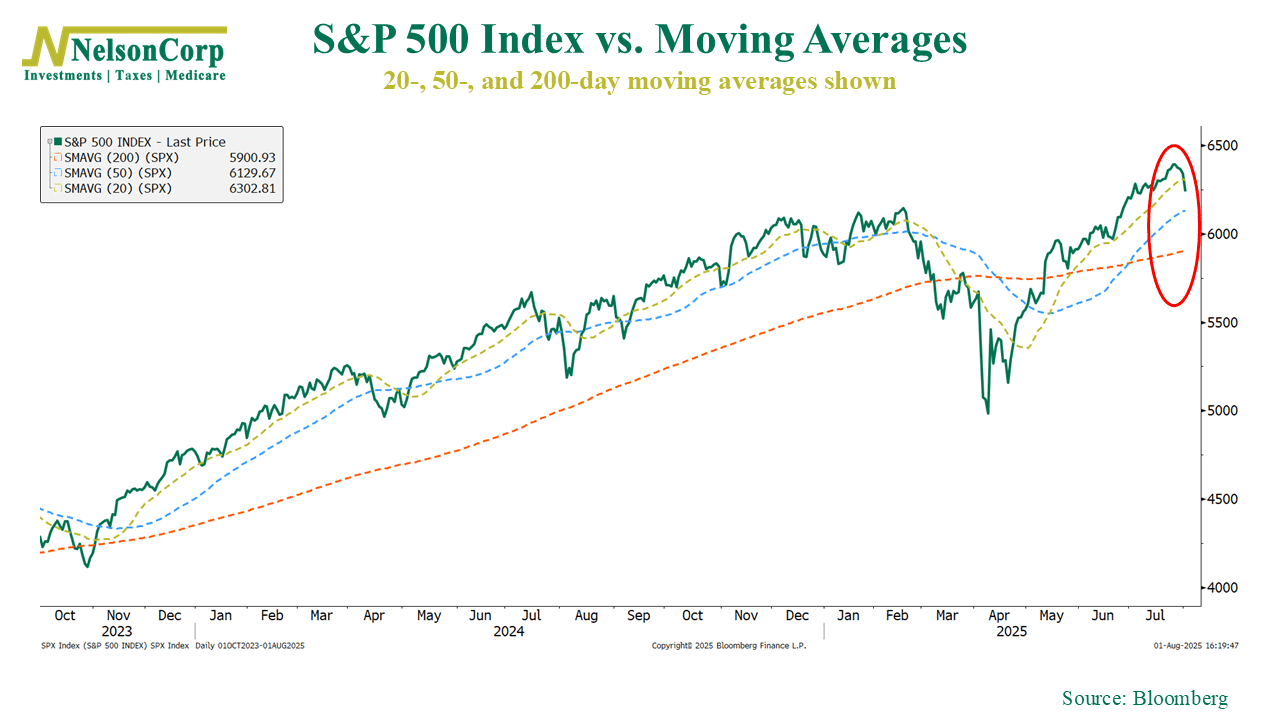

From a technical standpoint, the chart below shows that the S&P 500 is still cruising above both its 50- and 200-day moving averages. This is a good sign that the market’s broader trend is still holding strong, which is also the topic of this week’s Indicator Insights, which showed that the market’s long-term slope is pointing upward again.

But, as you might also notice from the chart, the S&P 500 did slip below its super short-term 20-day average last week. Obviously, this is nothing dramatic, but it does show that the market is taking a breather after a strong run.

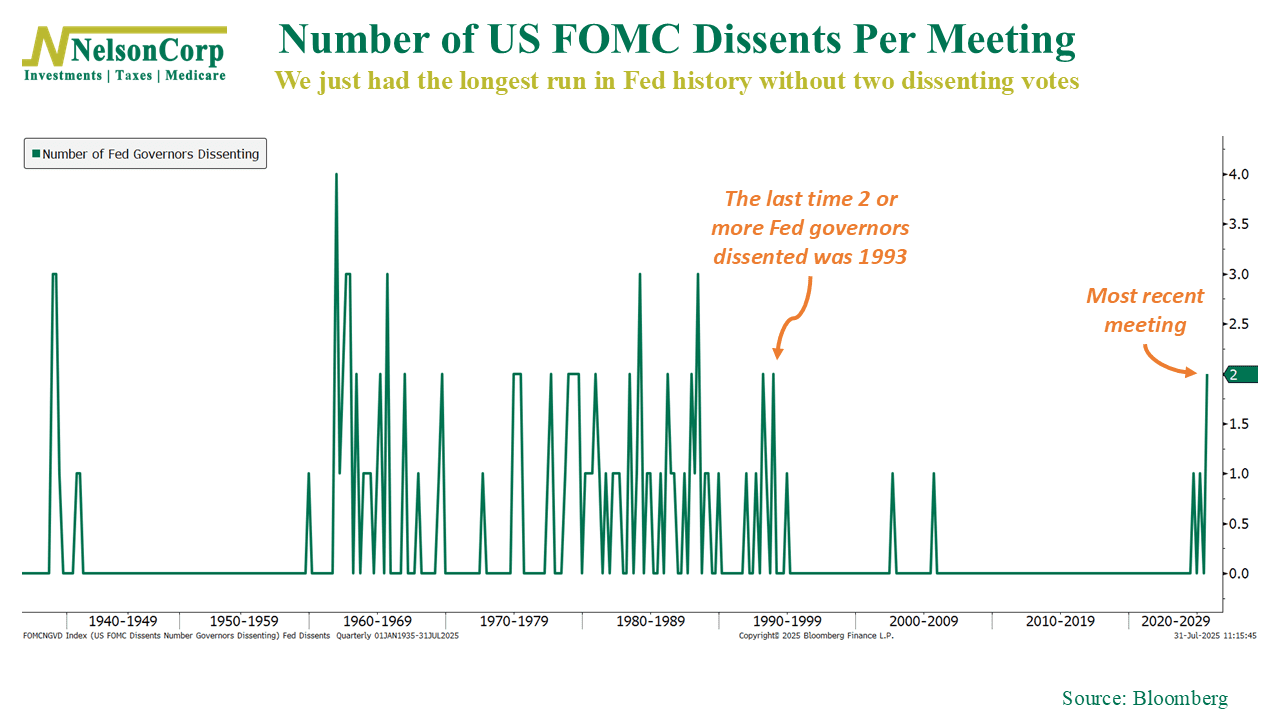

A bigger question looming over markets is the Fed. Rate cut chatter hasn’t gone away, and it picked up again after the most recent FOMC meeting, where two Fed governors broke ranks and dissented. That hasn’t happened since 1993. We featured that in our Chart of the Week because it could be a signal that opinions inside the Fed are starting to shift—and shifts like that often come right before major policy turns.

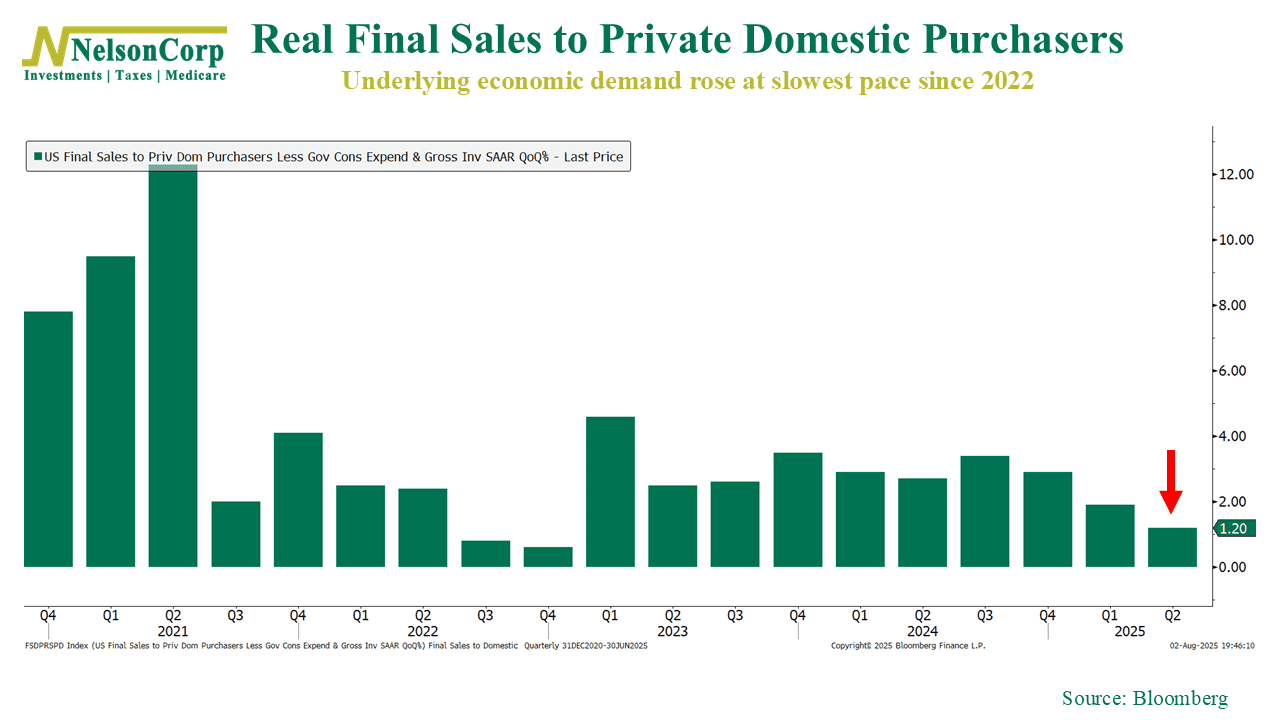

Of course, one area causing confusion at the Fed is economic growth. Is it strong or weak? Well, from a headline GDP point of view, growth still looks solid. It increased at a 3.0% annualized rate last quarter. But under the hood, things look a little softer. One key measure—real final sales to private domestic purchasers, shown below—came in weaker, hinting that consumer and business demand isn’t quite as strong as the GDP number suggest.

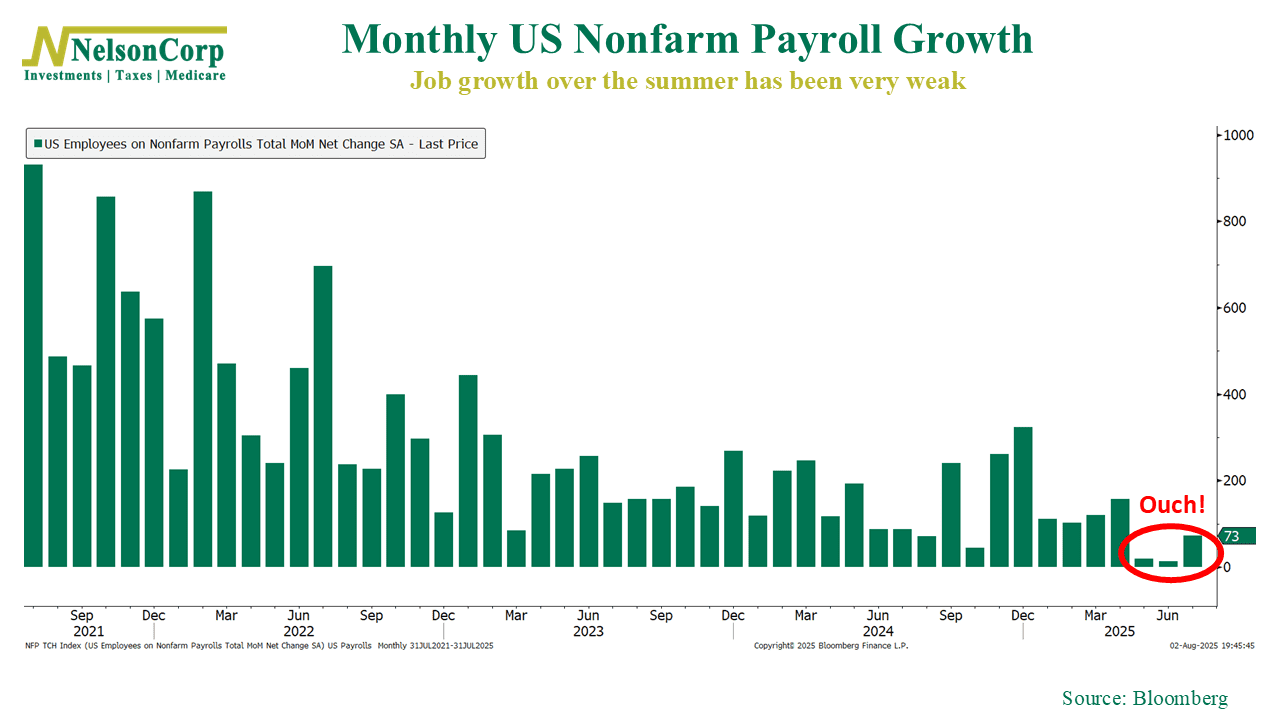

And then there is the labor market. We got a pretty big stinker of a jobs report last Friday. We only added 73,000 jobs in July, below expectations of more like 100,000. And the even bigger concern was the revisions to the May and June jobs numbers. They were revised lower to just 19,000 in May and just 14,000 in June.

Okay, that is concerning. But still, when we look at our broader models, the market’s internal price action remains strong, the macro backdrop is generally favorable, and investor behavior appears grounded. Those are all encouraging signals.

But of course, we’re always on the lookout for risks, and there was one indicator in particular that piqued my interest last week. It tracks the percentage of cyclical sectors—things like industrials, energy, and consumer discretionary stocks—in the S&P 500 that are doing well versus the broader market itself, and what it shows is that they have started to stall out recently.

As you can see, just one sector (Tech) is currently trading above its 50-day average. When leadership has gotten this narrow in the past, S&P 500 returns have turned negative. This is definitely something to factor into the equation when looking to put money to work in the short term.

Bottom line? I’d still answer the question, “how’s the market doing?” with “pretty good.” The big picture still looks solid. But under the hood, there are some signs of strain—so a little caution remains warranted.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The S&P 500 Index, or Standard & Poor’s 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.