OVERVIEW

Markets finished the week with solid gains across most major asset classes. The S&P 500 rose 1.72%, the Dow led large caps with a 2.30% gain, and the NASDAQ added 1.62%. Mid- and small-cap stocks posted even stronger results, with the S&P 400 climbing 2.85% and the S&P 600 jumping 3.24%. Value stocks outperformed growth, as the Russell 3000 Value Index gained 2.14%, compared to 1.62% for Growth.

International markets held steady. Developed international stocks (EAFE) inched up 0.04%, while emerging markets rose 0.25%. The U.S. dollar slipped 0.15% on the week.

Bond markets saw modest advances. Short-, intermediate-, and long-term Treasuries were mostly flat to slightly positive. High yield led the way with a 0.46% gain, followed by investment-grade bonds up 0.27%. Municipal bonds edged slightly lower, dipping 0.05%.

Commodities posted mixed results. Oil surged 2.61%, reversing some recent losses, and gold gained 1.68%. Corn also bounced back, rising 2.13%. Meanwhile, real estate added 1.73%, and the VIX ticked up slightly by 0.37%.

KEY CONSIDERATIONS

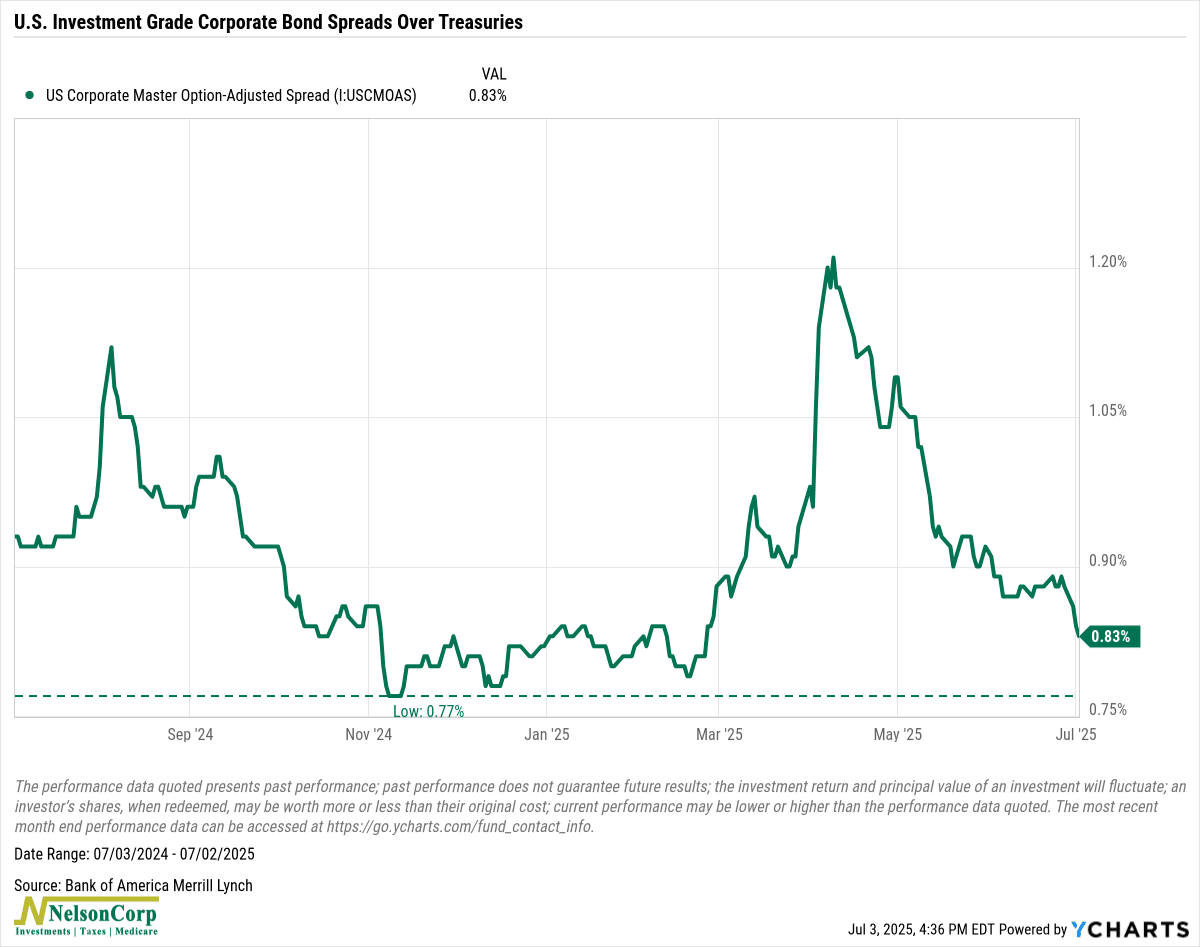

Keeping the Bulls in Check – While the S&P 500 grabbed headlines by pushing to new highs last week, the credit markets are sending a more measured message.

The following chart tracks investment-grade (IG) corporate bond spreads over Treasuries—a useful signal of how much extra compensation investors demand for lending to strong companies instead of the U.S. government. These spreads tend to widen when concern about the economy grows, and narrow when investors feel confident.

The latest reading clocks in at 0.83 percentage points. That’s still comfortably above the ultra-low levels we saw from November through February, when spreads hit a low of just 0.77 points. But it’s well below the early April spike, when spreads hit 1.20.

So what does that mean?

Unlike the stock market, which seems fully bought into the soft-landing story, credit markets aren’t acting euphoric. And in some ways, that’s a good thing. As we saw earlier this year, extremely low IG spreads can be a warning sign of complacency. When risks are ignored, the market tends to get caught off guard.

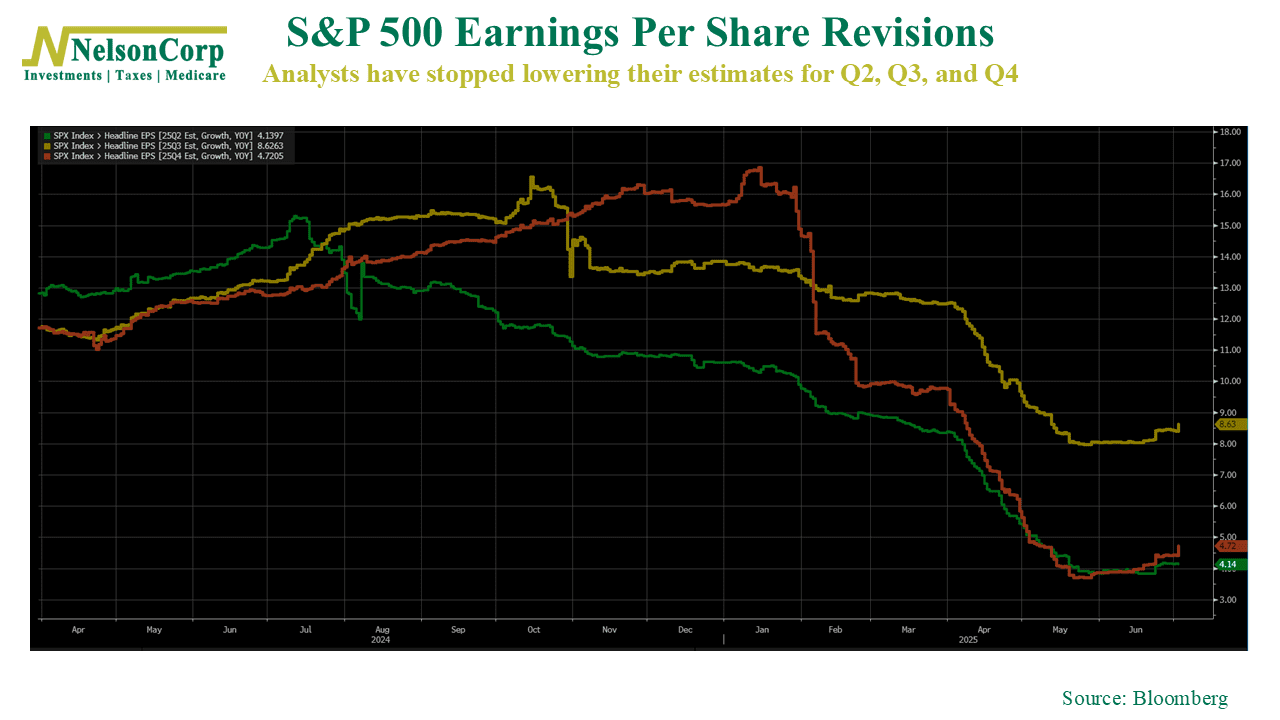

We’re seeing a similar dynamic play out in corporate earnings forecasts. After months of steady cuts, analysts have finally stopped lowering their estimates for Q2, Q3, and Q4 of this year. Expectations have stabilized, and that pause in downgrades suggests companies may now have a more achievable bar to clear. Even the modest downward revisions to 2025 earnings appear in line with long-term patterns—not a red flag, just business as usual.

In short, there’s still a layer of caution running underneath the market’s surface. And for long-term investors, that balance between optimism and realism might be exactly what’s needed right now.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The S&P 500 Index, or Standard & Poor’s 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.