OVERVIEW

Markets ended the week on softer footing, with U.S. equities broadly lower. The S&P 500 declined 0.44%, the Dow Jones Industrials fell 1.31%, and the NASDAQ dropped 0.95%. Large-cap stocks were under pressure as well, with the S&P 100 down 0.85% for the week. Year to date, performance remains mixed, with the S&P 500 up 0.49% while the NASDAQ is now down 2.47%.

Under the surface, leadership continues to favor value over growth. The Russell 3000 slipped 0.43%, with Growth falling 0.87% and now down 4.57% in 2026. Value held up better, rising 0.05% on the week and climbing to a 7.35% gain year to date. Mid- and small-cap stocks pulled back, with the S&P 400 down 0.88% and the S&P 600 off 1.50% last week, though both remain solidly positive for the year.

International markets remain a bright spot. Developed markets (EAFE) gained 1.22% and are now up 9.93% year to date. Emerging markets rose 2.77% for the week, pushing their 2026 advance to an impressive 14.69%, continuing to outpace most U.S. benchmarks. The U.S. dollar was little changed, down 0.04% on the week and up just 0.19% year to date.

Fixed income delivered steady results. Treasury returns improved as maturities extended, with short-term Treasuries up 0.07%, intermediate Treasuries rising 0.68%, and long-term Treasuries gaining 1.53%. Credit-sensitive sectors were mixed, as investment-grade bonds added 0.21% while high yield slipped 0.22%. Overall, bonds remain modestly positive in 2026.

Real assets continued to show strength. Commodities rose 1.67%, oil gained 1.36% and is now up 18.49% year to date, and gold climbed 3.29%, bringing its 2026 advance to 20.89%. MLPs added 0.62% and remain one of the strongest-performing areas this year, up 13.64%. Real estate rose 0.85% for the week. Meanwhile, the VIX jumped 4.03% and is now up more than 32% year to date, signaling a pickup in volatility despite pockets of strength across global markets.

KEY CONSIDERATIONS

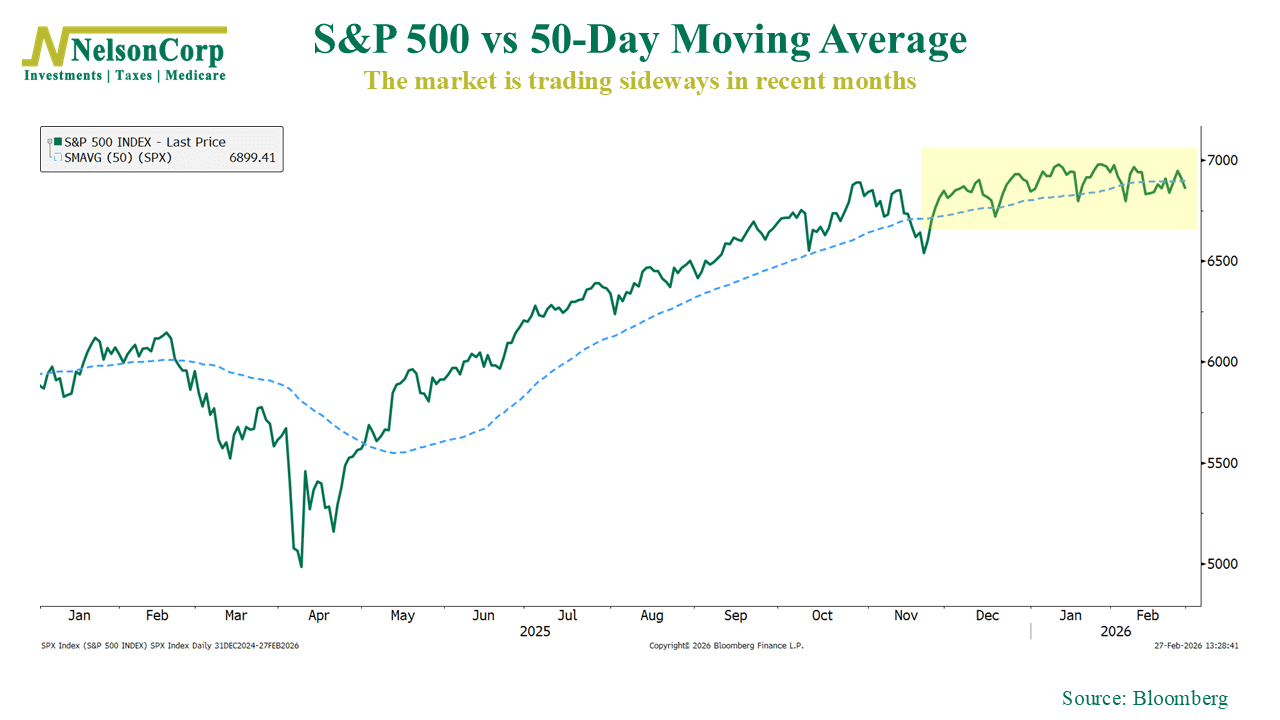

Mild Risk-Off – February was a somewhat bumpy month for U.S. stocks. Nothing crazy, but if you look at where the S&P 500 sits today, it’s essentially right in line with its average price over the past 50 days. In other words, we haven’t gone much of anywhere.

But that’s not the case for the entire market. Some areas are under real pressure. I’m looking at you, tech sector, particularly software.

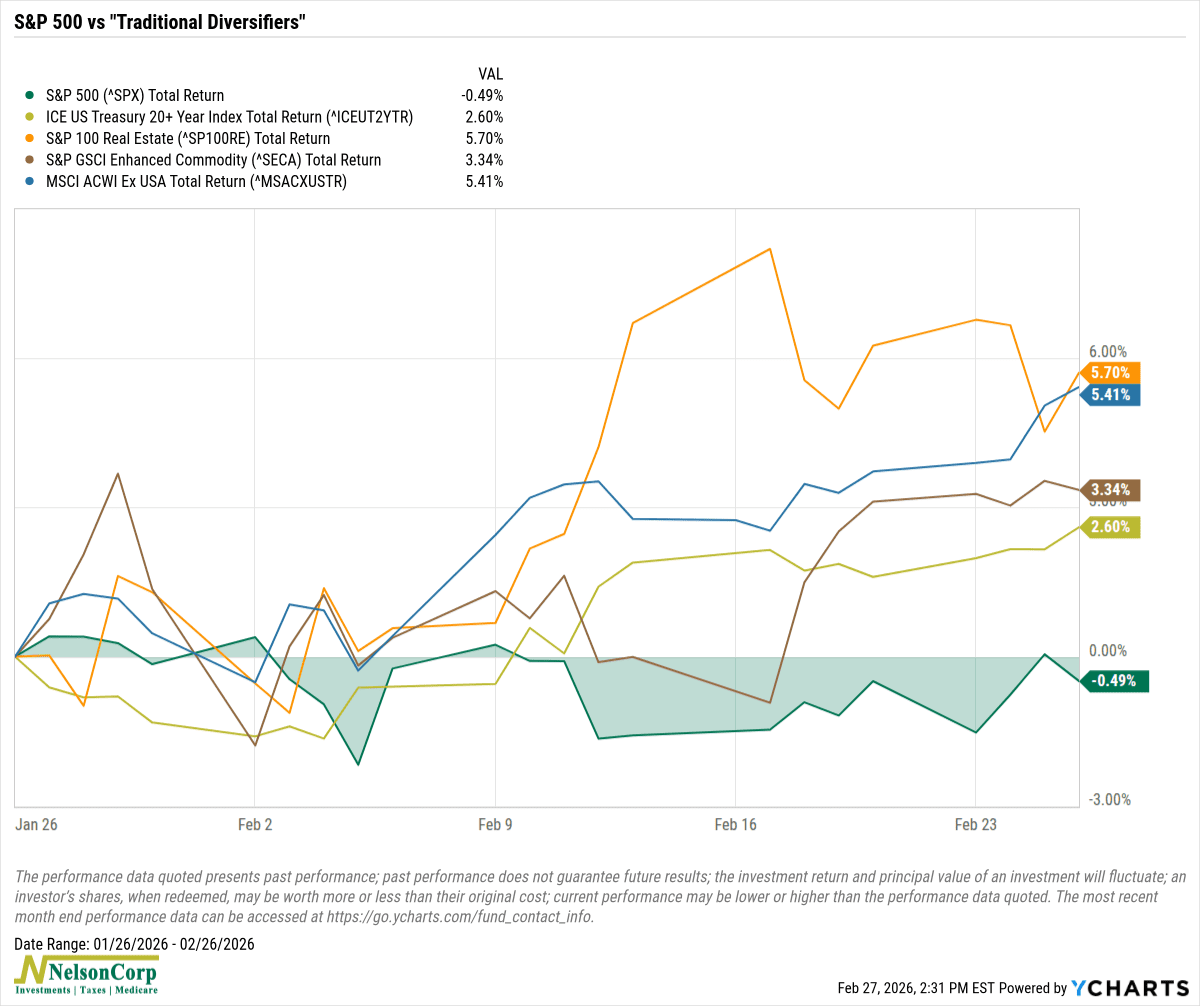

At the same time, though, other areas are holding up quite well. These are what you might call the traditional diversifiers, the asset classes that have historically helped smooth the ride when U.S. large-cap stocks stumble.

Think bonds, foreign stocks, real estate, and commodities. As the chart shows, many of these areas have outperformed over the past month, especially relative to the S&P 500.

It doesn’t always work this way. But right now, it is.

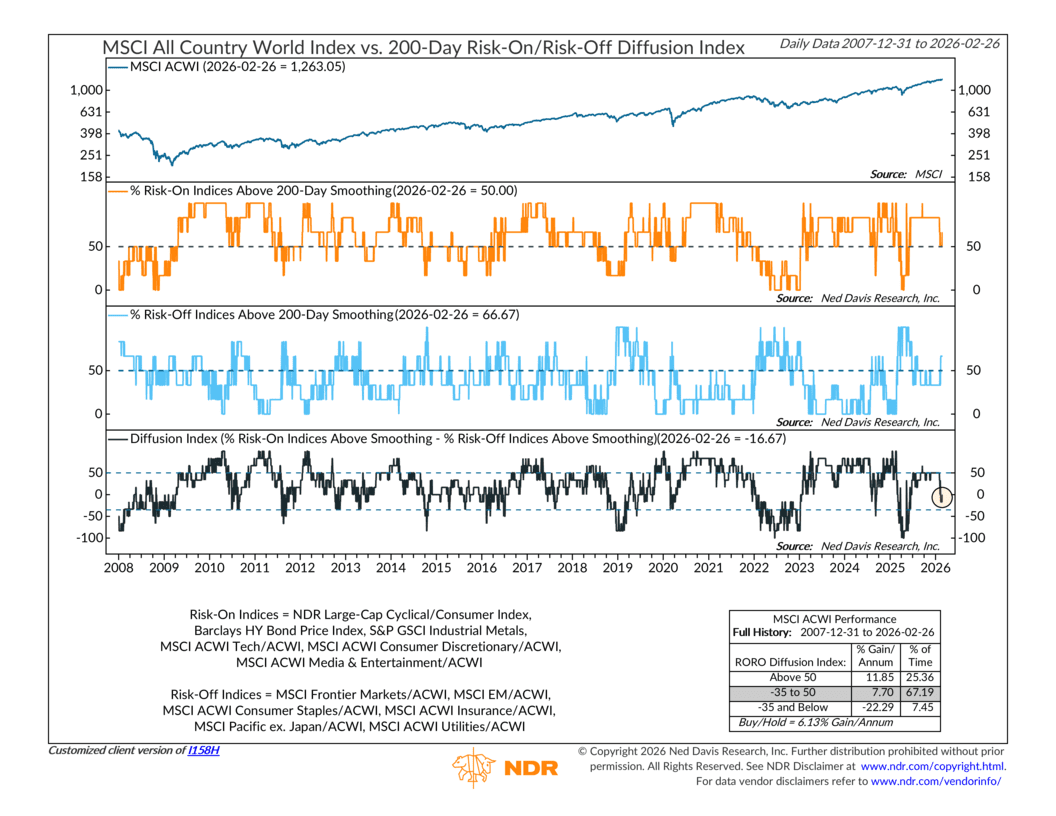

One reason is that the current financial landscape feels stuck in a Risk-On/Risk-Off limbo. Our indicator shows that 50 percent of Risk-On measures are trending higher, while roughly 67 percent of Risk-Off measures are trending higher. That nets out to a reading of negative 17 percent.

In plain English, the environment is leaning slightly risk-off, but not in a full-blown defensive panic.

That kind of backdrop can be supportive of traditional diversifiers. It also suggests we are not at contagion levels, where fear spreads broadly and correlations rise, dragging most asset classes down together.

So where does that leave us?

One key factor to watch in the coming weeks is how far this risk-off tone spreads. The more defensive sectors outperform, the more strain it can put on the broader market.

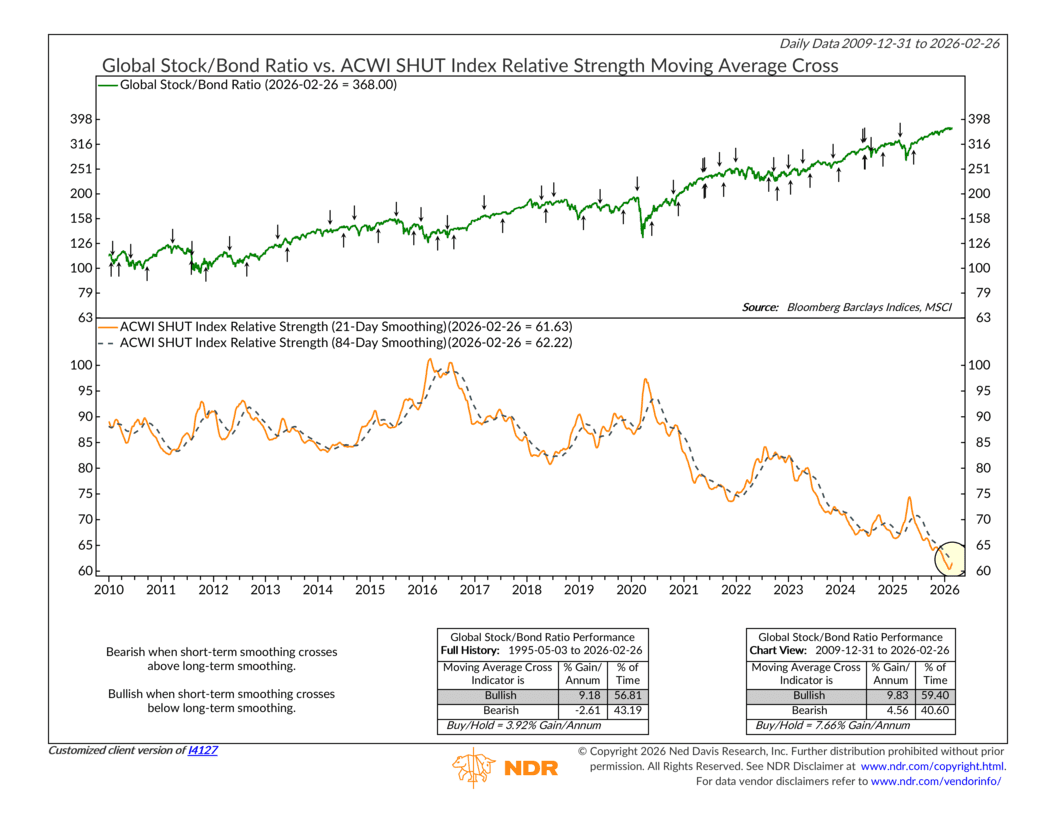

For example, the SHUT Index is a tool we use to track how much traditional defensive sectors are outperforming. SHUT stands for Staples, Healthcare, Utilities, and Telecommunications. The orange line on the chart measures SHUT’s relative strength versus the global stock market.

When that line is falling, SHUT is underperforming, which has been the dominant trend over the past five years. That trend could certainly continue. But we have started to see a small uptick recently. If that relative strength line crosses above its 84-day smoothing line, it would trigger a sell signal for the broader market. That is something worth monitoring closely.

The bottom line? We are in a market that is sending mixed signals. Diversification is working again, at least for now. But if defensive leadership continues to strengthen, it could be an early warning sign that this mild risk-off phase is turning into something more meaningful.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The S&P 500 Index, or Standard & Poor’s 500 Index, is a market-capitalization-weighted index of 500 leading publicly traded companies in the U.S.

The Dow Jones Industrial Average (DJIA) is a price-weighted index composed of 30 widely traded blue-chip U.S. common stocks. The Nasdaq 100 Index is a basket of the 100 largest, most actively traded U.S. companies listed on the Nasdaq stock exchange. The index includes companies from various industries except for the financial industry, like commercial and investment banks. The Russell 3000 Index is a capitalization-weighted stock market index that seeks to be a benchmark of the entire U.S. stock market. The S&P MidCap 400 is designed to measure the performance of 400 mid-sized companies, reflecting the distinctive risk and return characteristics of this market segment. S&P 600 Index measures the small-cap segment of the U.S. equity market. The index is designed to track companies that meet specific inclusion criteria to ensure that they are liquid and financially viable. The S&P 100 index is a capitalization-weighted index based on 100 highly capitalized stocks for which options are listed on the CBOE (Chicago Board of Exchange). The MSCI EAFE Index is an equity index which captures large and mid cap representation across 21 Developed Markets countries* around the world, excluding the US and Canada.

The Bloomberg U.S. Corporate Bond Index measures the investment grade, fixed-rate, taxable corporate bond market. The Bloomberg U.S. Corporate High Yield Index is comprised of domestic and corporate bonds rated Ba and below with a minimum outstanding amount of $150 million. The Bloomberg U.S. Municipal Index covers the USD-denominated long-term tax exempt bond market. The index has four main sectors: state and local general obligation bonds, revenue bonds, insured bonds and prerefunded bonds.