The Federal Reserve met this week for its first policy meeting under new Chairman Kevin Warsh. The decision to leave interest rates unchanged at 3.50%-3.75% was widely expected and didn’t come as much of a surprise. However, the message coming out of the meeting was a bit more hawkish than many investors anticipated.

Why? Well, because inflation has started moving higher again, reaching 4.2% year-over-year in May. The labor market remains relatively healthy, too. That combination makes it more difficult for the Fed to justify cutting rates anytime soon.

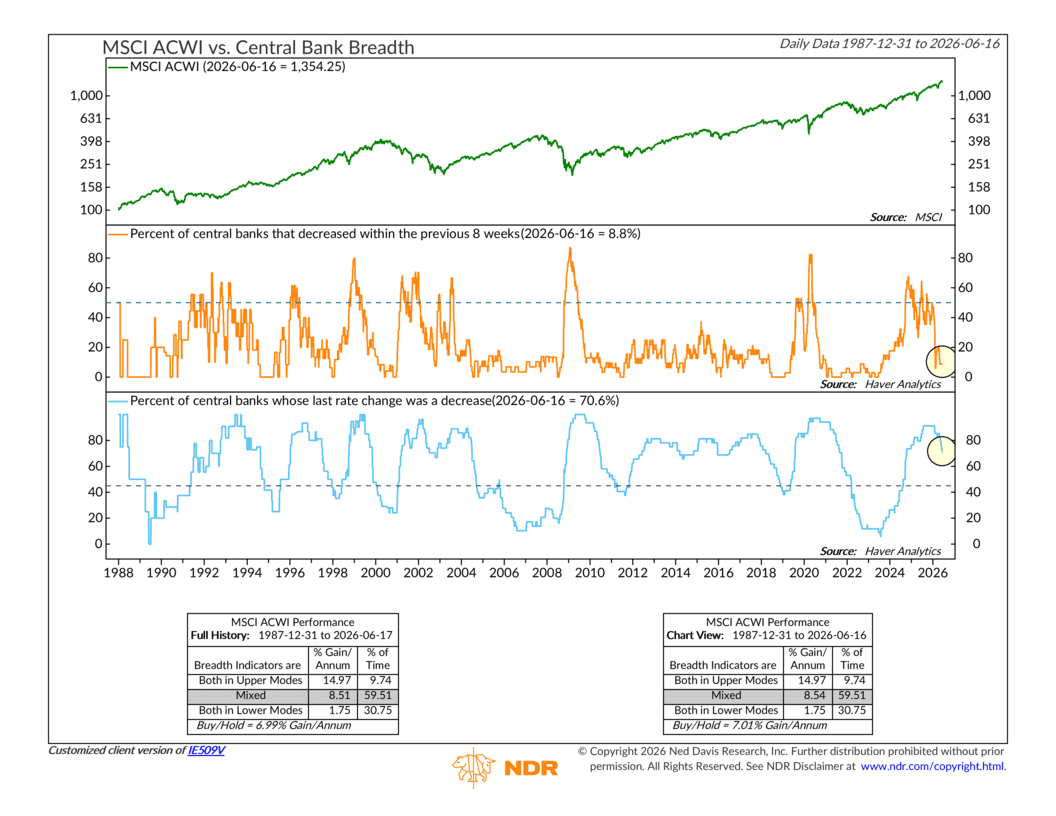

And the Fed isn’t alone. As our featured indicator this week shows, central banks around the world are beginning to shift in a more hawkish direction as well, meaning they’re starting to favor higher interest rates to fight inflation.

The indicator has three sections. The top panel shows the performance of global stocks, as measured by the MSCI All-Country World Index. The middle panel tracks the percentage of central banks that have cut interest rates within the past eight weeks. And the bottom panel shows the percentage of central banks whose most recent rate move was a cut.

A few things stand out. For starters, the bottom panel shows that roughly 70% of central banks last changed rates by lowering them. That’s still a bullish reading and suggests that most central banks remain in easing cycles.

However, that figure has fallen from a peak of roughly 91% earlier this year and continues to trend lower. More importantly, the middle panel shows that only 8.8% of central banks have actually cut rates over the past eight weeks. Near the end of last year, that number was closer to 50%.

So what does this mean for investors? The performance box at the bottom of the chart shows that when both indicators are in their most bullish zones, global stocks have historically returned about 15% annually. When the indicators are mixed, as they are today, average returns fall to roughly 8.5% per year. That’s still a positive environment for stocks and far better than the 1.8% annual returns seen when both indicators are in their weakest zones, but it does suggest that some of the tailwinds from global rate cuts may be beginning to fade.

Bottom line: Central banks are not slamming on the brakes, but they’re no longer pressing the accelerator as hard as they were a few months ago. The global rate-cutting cycle is still intact, but it’s clearly losing momentum, which could mean a more moderate return environment for stocks going forward.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The MSCI ACWI captures large and mid cap representation across 23 Developed Markets and 24 Emerging Markets countries. With 2,935 constituents, the index covers approximately 85% of the global investable equity opportunity set.