The writer Jason Zweig once wrote that regression to the mean is the most powerful law in financial physics. By this, he meant that after a period of really good stock market returns, we can expect things to cool down, and after a rough patch, there’s a good chance for improvement.

The historical record suggests he was right.

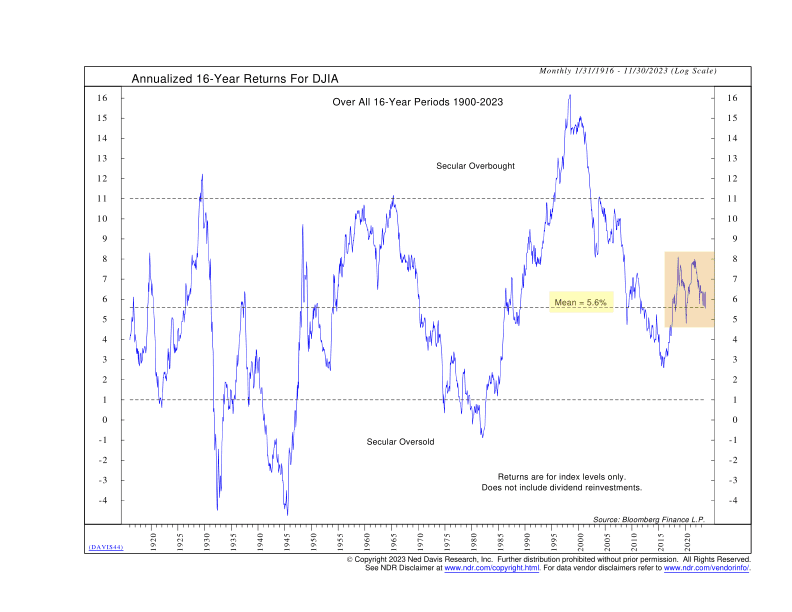

Our indicator above shows the annualized 16-year returns of the Dow Jones Industrial Average (the stock market) since 1900. In other words, the blue line shows what the Dow has returned annually over any given 16-year period (excluding dividends).

The dashed line through the middle represents the mean (or average) over the entire period. It’s 5.6%. In other words, the Dow has returned about 5.6% per year, on average, for every 16-year period over the past 123 years (again, that’s excluding dividends). Not bad.

But here’s where it gets interesting. You’ve probably noticed that the metric fluctuates quite a bit around that 5.6% average. In fact, very rarely is it actually at—or near—the average for very long.

For some points in history—like the 1930s, 40s, and 80s—the rolling 16-year return of the Dow is well below average, sometimes even negative. At these levels, the Dow is considered “secular oversold,” meaning returns have been unusually low compared to the historical average, making it primed to “revert to the mean” or do much better in the coming years.

There are other times, however—like the late 1990s/early 2000s—when the rolling 16-year return gets really high (secular overbought). When this happens, it tends to be a sign that stock returns have run up too high and, you guessed it, are therefore more likely to fall (or revert) down to the average.

In this sense, this indicator can be thought of as a valuation indicator, telling us how to think about the prospects of future stock returns based on current valuations.

What is the indicator saying now? The latest monthly reading showed that the Dow’s annualized 16-year return is just over 6%. That’s right in line with the long-run historical average. In fact, it has fluctuated between roughly 5% and 8% for more than half a decade now, which is interesting.

So, the bottom line is that the market is neither too high (overbought) nor too low (oversold) right now. It’s like Goldilocks – not too hot, not too cold, but just right. This might be reassuring for investors that despite the world’s craziness, recent stock returns have been relatively normal.

This is intended for informational purposes only and should not be used as the primary basis for an investment decision. Consult an advisor for your personal situation.

Indices mentioned are unmanaged, do not incur fees, and cannot be invested into directly.

Past performance does not guarantee future results.

The Dow Jones Industrial Average (DJIA) is a price-weighted index that tracks the performance of 30 major publicly traded companies in the United States.